Market Summary according to AFORTI: CPI and PMI decline, PLN stable, possible EUR and USD movements

The end of 2023 was quite calm on both global and Polish markets. The holiday season did not bring any important macroeconomic data that could have a significant impact on the market. The main activity on the market concerned closing positions before the end of the year, balance sheet settlements and achieving results on FX operations. We also did not observe increased activity of the NBP, which occurred already at the end of the year, in order to adjust foreign exchange reserves or correct exchange rates, which could affect the financial result of the Central Bank. We had the opportunity to see slightly more events at the beginning of 2024. It is true that the first week of the new year is usually characterized by reduced turnover and activity on financial and capital markets, hence we observed a decline in turnover on stock exchanges and a slight correction of the main indices. However, let's keep in mind that after sudden increases, such as we have seen recently both on WIG/WIG20 and global markets, such a correction is not strange.

Two pieces of information were most important from our market. The first one concerns the CPI inflation reading - which greatly surprised analysts - who expected significantly higher readings. The CPI value of 6.1% on an annual basis is significantly lower than the market consensus - where the expected value was in the range of 6.5-6.6%. This value is a decrease from the previous value of 6.6%. Despite the very good reading, the currency market did not record any major changes. This information obviously raises questions about potential decisions of the Monetary Policy Council at the next meeting. Taking into account the previous sharp reductions and the fact that the inflation target remains 2.5% (+/- 1 percentage point), it can be expected that the Monetary Policy Council will remain extremely cautious. Let us also remember that earlier decisions were made during the election campaign, which had a noticeable impact on the direction of changes. In our opinion, the Monetary Policy Council will leave rates unchanged at the next meeting, and the next inflation readings will be crucial for further decisions. It should be borne in mind that zero VAT on food has been extended until the end of the first quarter of 2024, and energy prices are subject to protective measures until the end of the second quarter of 2024. Due to these actions, further declines in inflation are possible, which are valued at 3.5 -4% at the end of the first quarter, but the restoration of the previous VAT rates on food will result in a rebound in the 3rd and 4th quarter to the level of approximately 5.5%. Therefore, the NBP/MPC will look at the inflation projections that will be published in March.

The second important information from the local market is the great interest in Polish debt. On Friday, the Ministry of Finance placed bonds in PLN at the auction, the value of which was approximately PLN 8 billion. Very important information is that interested parties submitted offers for twice this amount - i.e. nearly PLN 16 billion. The day before, bonds in EUR were sold. 10- and 20-year bonds worth EUR 3.75 billion quickly found buyers, and the reported demand amounted to EUR 10 billion. This shows that the Polish economy is currently appreciated by investors who are interested in constantly high profitability with decreasing risk. In the light of slowing inflation, this is an excellent opportunity for investors who value the risk of our market at an increasingly better level.

In light of the above data, the decline in the PMI index, which shows the mood among entrepreneurs, is somewhat surprising. The value, which still remains below 50, dropped from 48.7 to 47.4. This is certainly due to factors related to the uncertainty regarding the new decision regarding the declared support for entrepreneurs. So far, no specific details have been presented, but it must also be objectively noted that due to the holiday season, we can de facto talk about less than 10 days of real government activity in 2023. On the plus side, it should also be noted that the PMI index for Poland is still significantly higher than the reading in the Euro zone - which amounted to 44.4 in December.

January will also be important due to the need to adopt the budget by the end of the month and present it for signature by the President. Let us remind you that failure to obtain consensus and adopt the Finance Act on time will result in the dissolution of Parliament and the calling of early elections.

When it comes to currencies, we are dealing with rates remaining within our forecasted corridors. In the middle of the month, the zloty temporarily strengthened below EUR/PLN 4.3000, but the declines were corrected by significant demand from importers. We ended the year around 4.3500, which, given the current EUR/USD valuation, seems to be quite an optimal level balancing the expectations of importers and exporters. It is worth referring to the history of EUR/PLN quotations over the last two decades. The zloty moved in the EUR/PLN corridor of 3.2000-5.1000 against the common currency. The current level is therefore the middle of this range.

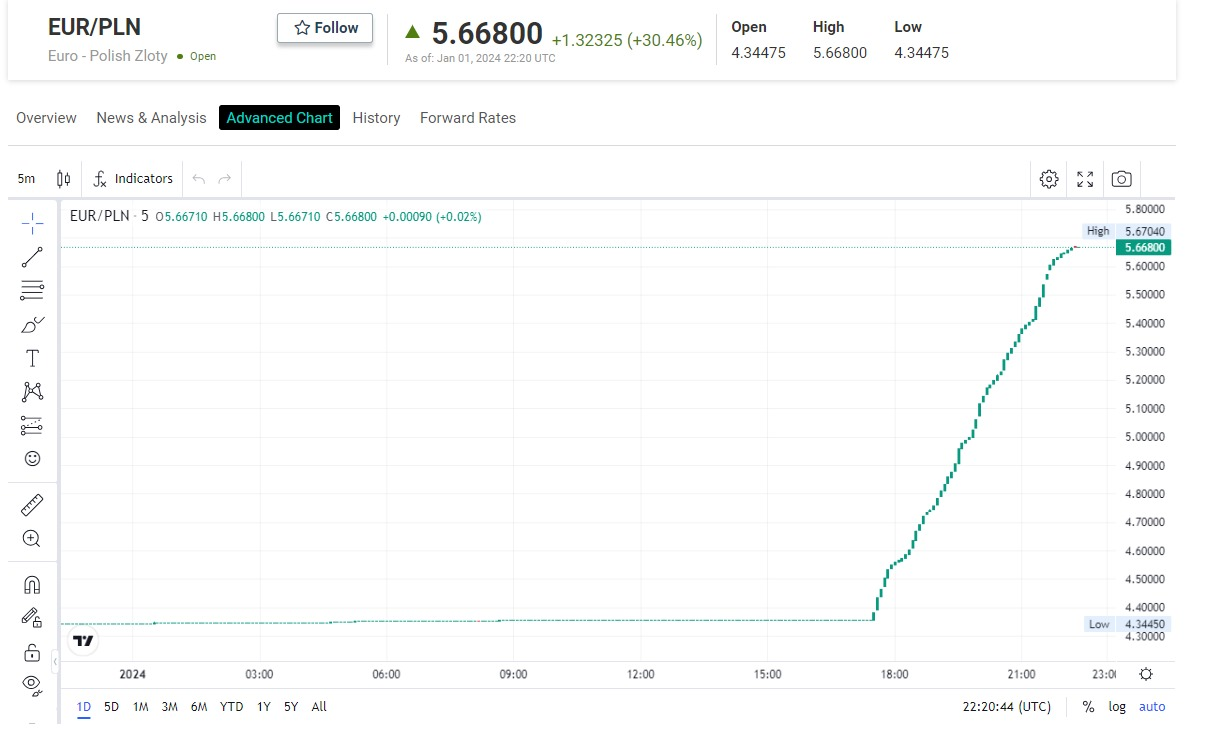

EUR/PLN over the last 30 days

Observing the current situation, our forecasts remain quite stable. The zloty currently does not have a strong potential to break levels below EUR/PLN 4.3000, but on the other hand, we do not see a strong signal to weaken above EUR/PLN 4.3650 in the coming week. We predict typical "range trading" in the 4.3200-4.3600 corridor.

Interestingly, it is also worth mentioning the bizarre jump in currency rates at the beginning of the year, which caused great surprise and disbelief. The zloty quoted at almost EUR/PLN 5.6700 was only a technical error by Google, which downloaded incorrect fixing data from the National Bank of Poland. The Ministry of Finance therefore issued an official inquiry and demanded explanations on how Google intends to avoid such situations in the future. The company is currently downplaying the situation. It is worth noting that both Bloomberg and Reuters published correct quotes, which fortunately cooled down the associated emotions.

Looking at the American currency, the dollar, which until mid-December remained above the psychological level of USD/PLN 4.0000, after the correction on EUR/USD, rapidly lost against the zloty, initially reaching the level of USD/PLN 3.9200, and after corrections to around 3.9750, again headed south to reach the USD/PLN level of 3.8850 in the last days of 2023. Then we had a correction that brought the rates to around USD/PLN 4.0000. However, the resistance was very strong and ultimately the quotes were 3 cents lower.

USD/PLN over the last 30 days

With the correction on EUR/USD, we expect that the dollar will be in the 3.9450-3.9800 corridor in the next week. Of course, the behavior of the quotes of the main currency pair EUR and USD will be crucial.

However, looking at the EUR/USD quotations, in recent days we have seen quite strong movements on the market. The dollar strengthened quite significantly - from the initial levels reaching EUR/USD 1.1130, we observed a correction to around 1.0900. The dollar was certainly supported by weaker than expected results from the European economy. The previously mentioned low PMI, disappointment with inflation readings that turned out to be worse than expected, as well as corrections in bond yields above 4% (in the US). Although we were not dealing with "first-rate" data, the United States was clearly gaining compared to the European economy, which was still in stagnation. The latter clearly cannot gain momentum, and the pressure of the Chinese economy, which is clearly not subject to the quite restrictive regulations that apply to European countries, is becoming more and more felt.

Looking at the commodity markets - especially BRENT crude oil - we are dealing with consolidation around USD 77-78/barrel. Concerns about the further escalation of the conflict in the Middle East and the continuing war in Ukraine certainly do not encourage the market to calm down, and the current level shows that breaking the level of USD 70 per barrel is quite distant in time.

BRENT crude oil – last month USD/barrel

Gold – still remains an attractive

asset. After quite strong increases to around USD 2,080, we observed a

correction, but the precious metal still remains above USD 2,050 per ounce,

which suggests that investors value the stability associated with investing in

certain assets.

Finally, a short look at the stock

markets. There is exceptional optimism on the Warsaw Stock Exchange. The WIG

index reached almost 80,000 at the end of the year. The initial correction

at the beginning of the year is quite natural, but according to analysts it

should not disturb further growth. Moreover, some analysts predict that 2024

may bring index values of 100,000. This would be an exceptional increase,

but looking at previous increases in 2023 - it does not seem impossible. On

WIG20, the level of 2.360 was corrected and is currently 2.275, but we can

expect that after a temporary correction, the increase will continue.

Szymon Jańczak

Director of the Treasury Department

AFORTI.BIZ